When to Use Leverage?

Strategies for Balancing Risk and Reward in a Turbulent Financial yet Exponential Technological Landscape

Introduction

In the late 1970s and early 1980s, the world faced a tumultuous economic period marked by geopolitical upheavals, drastic changes in the global financial system, soaring interest rates, and rampant inflation. In addition to the ongoing Cold War, the Iranian Revolution and the Soviet invasion of Afghanistan sent shockwaves through the oil markets, while the collapse of the Bretton Woods system and the rise of floating exchange rates fundamentally altered the international monetary landscape. In the United States, the Federal Reserve, led by Paul Volcker, embarked on a bold campaign to combat inflation by raising interest rates to unprecedented levels, triggering a deep recession and a debt crisis in developing countries.

Fast forward to 2024, and we find ourselves in a striking similar situation. Geopolitical tremors, including conflicts in Ukraine, the Middle East, and tensions in the South Chinese Sea are creating economic instability. The global financial system is still grappling with the aftershocks of a global pandemic, escalating geopolitical tensions, and supply chain adjustments. Inflation remains stubbornly high, prompting central banks to raise interest rates, which in turn increases the cost of borrowing.

In addition, a looming US debt crisis, coupled with the specter of rising inflation, has raised concerns about the stability of the US dollar and its role as the world's reserve currency. Amidst this backdrop, we are witnessing the rise and convergence of exponential technologies, such as artificial intelligence, which hold the promise of transforming industries and driving productivity gains.

In this context, the question of when and how to use leverage to acquire productive and well-managed businesses becomes increasingly relevant. History has shown that owning such businesses can serve as a powerful hedge against inflation, as they possess the ability to generate strong cash flows and maintain pricing power in the face of rising costs

This essay aims to answer this critical question by examining the factors that investors must consider when deploying leverage in the current economic environment, drawing on lessons from the past and the unique challenges and opportunities presented by the present.

We believe that leveraging debt can be a powerful tool for growth, but it must be employed judiciously, especially in times of economic uncertainty. By examining the interplay between technological disruption, geopolitical risk, and the evolving financial landscape, we aim to provide a framework for making informed decisions about the strategic use of debt in acquiring businesses that can thrive in an inflationary environment. Through a combination of historical analysis, case studies, and forward-looking insights, this essay seeks to equip investors with the knowledge and tools necessary to navigate the complexities of the current investment landscape and position themselves for long-term success.

The Economic Environment

The global economy is facing a perfect storm of challenges, with the looming US debt crisis, high inflation, and rising interest rates converging to create an environment of unprecedented uncertainty. At the heart of this crisis lies the US government's reliance on debt to finance its spending, pay off maturing obligations, and cover interest payments. With the national debt surging to $34.7 trillion in May 2024, the sustainability of this approach is being called into question.

The US government's position as the largest buyer and owner of its own debt, facilitated through the Treasury's buyback program and the Federal Reserve's quantitative easing, has effectively created a situation where the government is printing money to purchase its own debt. This self-reinforcing cycle has ignited an inflationary spiral, with inflation levels reaching heights not seen in decades. As Warren Buffett once remarked, "You can bet on inflation," and the current economic environment is a testament to this prescient observation.

To combat rising inflation, the Federal Reserve has taken aggressive action, raising interest rates to levels not seen since 2007. While intended to curb borrowing and spending, these high interest rates have had the unintended consequence of increasing the government's debt service costs. This, in turn, necessitates further debt issuance, leading to even larger budget deficits and perpetuating a vicious cycle that becomes increasingly difficult to break.

Implications

The implications of the US debt crisis and the resulting inflation extend far beyond the borders of the United States. As the world's largest economy and the issuer of the global reserve currency, the US dollar plays a pivotal role in international trade and finance. Major economic powers such as Japan and China, the two largest foreign holders of US debt, are particularly vulnerable to the inflationary pressures emanating from the United States. A weakening US dollar and rising inflation could have significant repercussions for these economies, as well as for the countless other nations that rely on the dollar for their international transactions.

High inflation and rising interest rates will also have direct consequences for borrowing and leveraged acquisitions. Higher interest rates increase the cost of borrowing, making debt financing more expensive for companies pursuing acquisitions or companies that have to make investments as part of a necessary transformation process to survive in the future.

This is particularly challenging for leveraged buyouts (LBOs), which rely heavily on debt. With approximately $300 billion in leveraged loans maturing between 2024 and 2026, many borrowers will face higher refinancing rates, potentially leading to a rise in dislocated capital structures. Some borrowers may explore alternative financing options, such as private credit or amend-and-extend arrangements, while others may opt for M&A exits if a vanilla refinancing is unachievable. The higher cost of debt will likely result in lower debt multiples and a more conservative approach to leveraged acquisitions, as investors and lenders must carefully assess the cash flow generation and debt servicing capacity of target companies.

The direct impact on businesses and investments will vary depending on the sector and company-specific factors. Sectors with stable cash flows, inelastic demand, and the ability to pass on cost increases to consumers, such as healthcare, utilities, and consumer staples, may be better positioned to handle higher leverage and secure acceptable refinancing terms. However, industries sensitive to economic cycles, such as discretionary consumer goods, travel, and luxury products, may face reduced demand and declining revenues, making it difficult to service debt.

Businesses with high fixed costs or exposure to commodity price fluctuations may also struggle to manage leveraged balance sheets. While rising interest rates can erode the real value of debt over time, potentially benefiting highly leveraged firms, they also put pressure on margins and cash flows, making it harder to service debt.

Technology companies, particularly those in high-growth sectors, are a category for themselves. Driven by innovation and rapid scaling, these companies often prioritize growth over profitability, investing heavily in R&D, talent acquisition, and market expansion. However this strategy relies on access to readily available cheap capital, which becomes more challenging in a high-interest-rate environment. This is particularly challenging for companies that have high burn rates and have not yet achieved stable cash flows and profitability, as they may struggle to raise additional rounds of funding at favorable valuations.

Great Businesses as an Inflation Hedge

Warren Buffett offers a simple yet powerful prescription for thriving in an inflationary environment: invest in well-run businesses with strong pricing power and low capital requirements.

Buffett's approach is rooted in the belief that the best inflation hedge is a company that produces a high-quality product or service, requires minimal capital investment to grow, and has the ability to pass on cost increases to its customers. These businesses generate consistent cash flows and are able to maintain their profitability even in the face of rising input costs. By investing in such companies, investors can effectively insulate themselves from the erosive effects of inflation and position their portfolios for long-term success.

Conversely, Buffett cautions against investing in businesses that require significant ongoing capital expenditures to maintain their operations, while offering little in the way of real returns. These capital-intensive businesses are particularly vulnerable to inflationary pressures, as they face the dual challenges of rising input costs and the need for continuous investment just to stay afloat. In an inflationary environment, such businesses can quickly see their profitability erode, leaving investors exposed to significant losses.

Beyond Buffett’s value approach, we believe that companies directly involved or indirectly benefiting from exponentially improving technologies may also offer a promising inflation hedge. The rapid advancement and convergence of technologies such as artificial intelligence, robotics, and biotechnology are fundamentally reshaping industries and creating new opportunities for value creation. Companies that effectively develop and harness these technologies to drive innovation, improve efficiency, and create new markets are well-positioned to outpace inflation and deliver – over the long-term – strong returns to investors willing to take well calculated risks.

Leveraged Acquisitions

If the best hedge against inflation is either investing in a business that is at the cusp of developing the cutting-edge technology of tomorrow or owning business that is cash-flowing with strong pricing power and low capital requirements – ideally participating in the exponential growth of the former – when is it appropriate to use leverage to finance the acquisition?

While high-growth technology companies are usually funded without leverage by VC funds which themselves raise capital from limited partners, the acquisition of highly profitable businesses have been funded traditionally largely by debt, as debt financing allows the acquirer to leverage their capital and generate higher returns on equity. However, in an environment of rising inflation, rising interest rates, and tightening credit conditions, the calculation around using debt to finance acquisitions becomes more complex.

Over the past 100 years, leveraged buyouts (LBOs) became a popular method for acquiring cash-flowing businesses, particularly by private equity firms. In an LBO, a significant portion of the acquisition price is financed through debt, with the target company’s assets and future cash flows serving as collateral. The debt is typically structured as a combination of senior debt, which has priority repayment, and subordinated debt, which carries higher interest rates but provides additional flexibility.

A Historical View

The history of debt used in acquisition transactions can be traced back to Andrew Carnegie, a pivotal figure in the steel industry. During the 1860s, Carnegie began investing in railroad companies, which were heavily reliant on debt financing for their expansion and operations. His strategy often involved buying railroad bonds, which are a form of debt investment, and then leveraging these investments to gain control or significant influence over railroad companies.

While Andrew Carnegie was not directly involved in leveraged buyouts as we know them today, his 1901 sale of Carnegie Steel Company to J.P. Morgan for $480 million is considered to be one of the first major buyouts in American history.

The first “real” leveraged buyouts happened during the 1950s and 1960s, with early notable transactions including McLean Industries’ acquisition of Pan-Atlantic Steamship Company in 1955 and Lewis Cullman's acquisition of Orkin Exterminating Company in 1964. However, LBOs only gained significant popularity in the 1980s, fueled by the rise of junk bonds pioneered by Michael Milken of Drexel Burnham. This era saw iconic deals such as KKR's acquisition of RJR Nabisco in 1989, which was the largest LBO at the time. The success of these high-profile transactions, coupled with the availability of cheap debt and a favorable regulatory environment, contributed to the growth and mainstream acceptance of LBOs as a powerful takeover strategy.

Most interestingly, the first wave of leveraged buyout transactions began in the 1980s, an inflationary environment with high interest rates, propelled by the emergence of high-yield “junk” bonds, a financial innovation spearheaded by Michael Milken. However, this era was marked by excessive speculation and lax lending practices, resulting in overpriced acquisitions and the eventual collapse of the high-yield bond market. The high interest rates prevalent during this period further compounded the challenges faced by LBOs, as the increased cost of debt financing heightened the risk of default for highly leveraged companies. Notably, some of the most prominent LBOs of the time, such as KKR's acquisition of RJR Nabisco in 1989, ultimately led to significant losses. While inflation can potentially benefit highly leveraged companies by eroding the real value of debt over time, it also exerts pressure on portfolio companies' margins and cash flows, making it more difficult to service their debt obligations.

During the 1980s, LBO debt typically took the form of senior, secured loans arranged by banks or investment banks, with junk bonds providing supplementary financing. In comparison to contemporary practices, debt covenants during this period were more stringent, and lenders exercised greater control. The LBO boom of the 1980s came to an end due to a confluence of factors, including the re-enactment of anti-takeover laws, mounting political pressure against high leverage, the junk bond market crisis, and a credit crunch, with many LBOs from this era ultimately succumbing to bankruptcy.

When to use Leverage?

As we’ve argued, the economic and investment landscape of the 1970s and 1980s shares characteristics with the current landscape. This underlines the importance of carefully considering the use of leverage in current and future acquisition strategies to avoid high-profile bankruptcies and losses investors have seen during the 1980s.

This leaves us with the central question: when is it appropriate to use debt to acquire businesses, and how much leverage is optimal?

Ultimately, the use of debt is always related to risk. Morgan Housel, in his blog article “How I Think About Debt”, gave the example of Japanese “Shinise” businesses; these are the 140 businesses in Japan that are still operating more than 500 years after they were founded, a few of them more than 1,000 years old. These businesses are still operating after dozens of wars, emperors, catastrophic earthquakes, tsunamis, depressions, and so on. Morgan Housel highlighted that all Shinise businesses share one common characteristic: they hold tons of cash, and no debt.

This reminds of Warren Buffett’s approach at Berkshire Hathaway, who used acquisition debt and leverage highly cautiously and in a disciplined manner over the years. Berkshire Hathaway now holds over $28 billion in cash and $153 billion in short-term U.S. treasury bills as of Q1, 2024. With his principle of maintaining a “Fort Knox” balance sheet, Buffett has positioned Berkshire Hathaway to weather the severest economic downturns and capitalize on opportunities that arise during times of market dislocation.

All else being equal, companies that are indebted are more likely to run into problems than those that aren’t. The presence of debt within a company's capital structure introduces a significant level of risk that cannot be overlooked. By obligating the firm to make regular interest payments and repay the principal, regardless of financial performance or economic conditions, debt creates an inflexible commitment that can quickly become a burden during times of distress. Consequently, highly leveraged companies find themselves vulnerable to the ever-present dangers of financial distress, default, foreclosure, and bankruptcy, which can threaten not only the company's survival but also the interests of its stakeholders. While debt can be a powerful tool for growth when used judiciously, its presence inherently amplifies risk.

Or in Warren Buffett’s words, you should always play tomorrow: “Do not go broke, no matter what happens. So, keep plenty in reserves, and go low on debt.”

Does that mean that all debt is bad and that debt should be avoided at all costs?

Absolutely not.

Debt can be a powerful tool for growth and expansion. Whether debt is appropriate depends on the company's size and its ability to withstand potential fluctuations in profitability and asset value.

However, as Morgan Housel illustrates with the example of Shinise enterprises, the level of indebtedness directly impacts a company's resilience to various forms of volatility, including economic recessions, market downturns, and unexpected events.

As debt levels increase, the range of volatility a company can survive narrows, until at excessive levels of debt, only the most stable and predictable business environments are manageable. Therefore, the key to effectively utilizing debt lies in striking a balance between the benefits of leverage and the risks associated with heightened financial fragility.

Risk and Volatility

In his memo “The Impact of Debt” Howard Marks, the co-founder of Oaktree Capital Management, emphasizes that excessive leverage exposes investors to the risk of ruin and that the appropriate level of leverage is directly tied to the riskiness and volatility of the underlying assets.

Stable, predictable assets can withstand higher levels of debt, while riskier, more volatile assets necessitate a more conservative approach to leverage.

The allure of leverage lies in its ability to amplify returns IF investments perform well. By employing debt capital, which is typically cheaper than equity, investors can acquire a larger pool of assets and potentially generate higher profits. However, as Marks cautions, this upside potential is accompanied by a corresponding downside risk: when asset values decline, the more leverage employed, the greater the equity loss.

A prime example of the perils of excessive leverage can be found in the aforementioned LBO boom of the 1980s. Fueled by the availability of high-yield "junk" bonds and loose lending practices, many LBOs were financed with unsustainable levels of debt. When the economic environment deteriorated, highly leveraged companies like RJR Nabisco struggled to service their debt obligations, leading to a wave of bankruptcies and losses for investors.

Even if losses are not permanent, a downward fluctuation in asset values can trigger a cascade of events for highly leveraged portfolios, including lenders cutting off credit, investors withdrawing equity, or regulatory violations forcing asset sales.

One of the largest risks with leverage are tail events. While historically “normal” levels of volatility are accounted for in investor’s calculations, it is the infrequent but extreme “tail events” that can saddle leveraged investors with catastrophic losses. The problem is that as time passes without such events happening, the perceived risk diminished, leading to a false sense of security which in turn leads to a higher willingness to take on excessive leverage – often just before the next crisis strikes.

This is true on both sides: lenders and borrowers. As time passes, lenders and borrowers become overconfident in “average” forecasts as they get used to the favorable aspects of leverage, overlooking the negative potential. This leads to investors more interested in employing more debt, and lenders willing to provide more, while regulations of the use of leverage become more permissive. Only to be crushed by the fragility of leverage as soon a tail event appears.

Howard Marks quotes Nassim Taleb from his book “Fooled by Randomness” which I want to borrow, as it fits so perfectly:

Reality is far more vicious than Russian roulette. First, it delivers the fatal bullet rather infrequently, like a revolver that would have hundreds, even thousands of chambers instead of six. After a few dozen tries, one forgets about the existence of a bullet, under a numbing false sense of security [...] Second, unlike a well-defined precise game like Russian roulette, where the risks are visible to anyone capable of multiplying and dividing by six, one does not observe the barrel of reality [...] One is thus capable of unwittingly playing Russian roulette – and calling it by some alternative “low risk” name.” (Nassim Taleb; Fooled by Randomness, p. 28)

Using Leverage Prudently

The optimal use of leverage is about balance, not excess. While leverage can amplify returns when investments perform well, it also magnifies losses during downturns. Given this dual nature, the inclination to maximize leverage based on optimistic projections is misguided. Investors must consider both the potential for amplified losses and the existential risk of ruin in adverse scenarios.

As Howard Marks puts it, ”determining the proper amount of leverage has to be a function of optimizing, not maximizing.” Given that, the optimal amount of debt is typically less than the maximum amount one has access to.

The closest one can get to choosing the optimum level of leverage is one where one calculates the investment returns – based on demonstrably cautious assumptions – not for maximum returns but rather satisfactory ones.

By definition, if one is doing something novel, unproven, risky, or volatile, one should never seek to maximize returns but optimize to survive at all cost. This key to survival is what Warren Buffett constantly insists on: the margin of safety.

In the words of Howard Marks: “The riskier the underlying assets, the less leverage should be used to buy them. Conservative assumptions on this subject will keep you from maximizing gains but possibly save your financial life in bad times.”

Leverage is a magnifier, when used judiciously, it can amplify returns, but it also magnifies risks. Therefore, it is crucial to employ leverage based on conservative assumptions, particularly when dealing with novel, unproven, or inherently risky ventures. Warren Buffett's emphasis on a 'margin of safety' is pertinent here; leveraging to the maximum often conflicts with ensuring survival during downturns.

Leverage should not be seen as a panacea or a tool to transform low returns into high ones, as was commonly attempted during 2003-2007. Instead, it should be applied wisely to suitable assets and under conditions where the risk premium justifies its use. Particularly, leveraging in the trough of an economic cycle is generally safer than during prolonged periods of asset appreciation. In essence, leverage is a powerful but double-edged tool that must be handled with utmost care and respect.

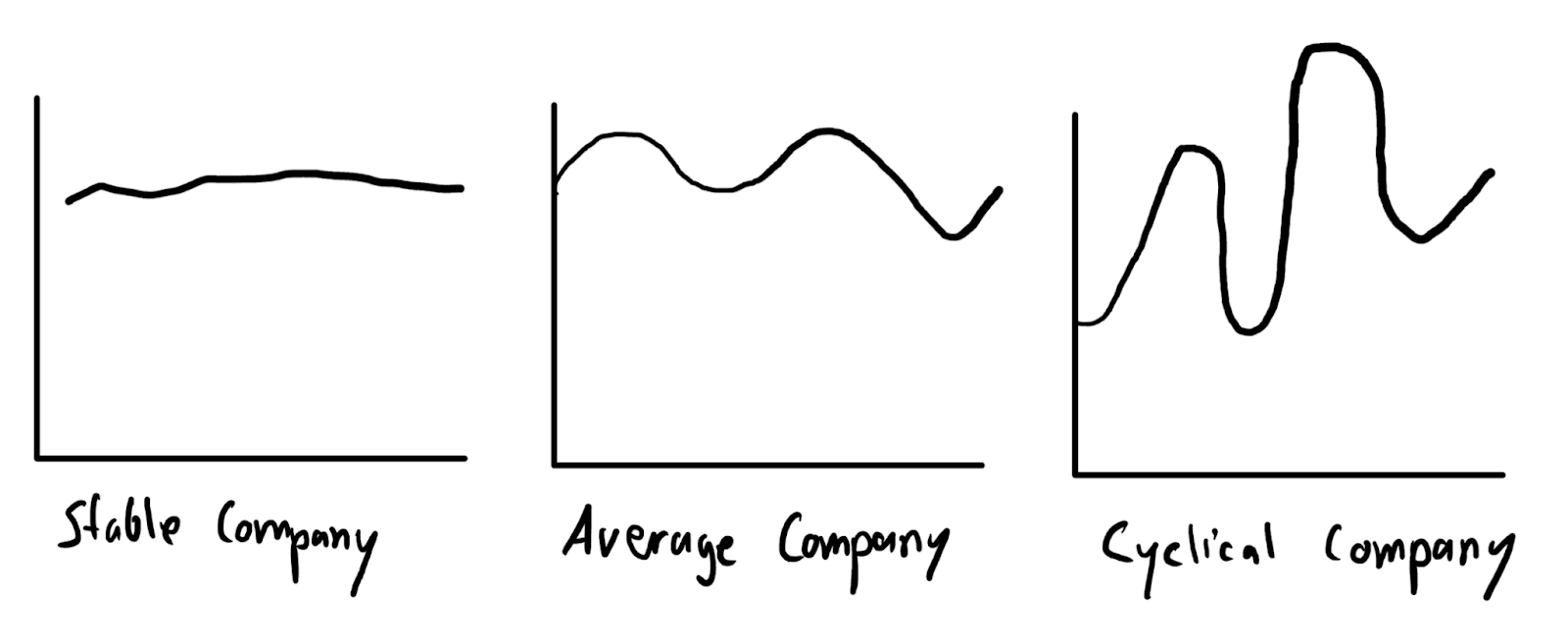

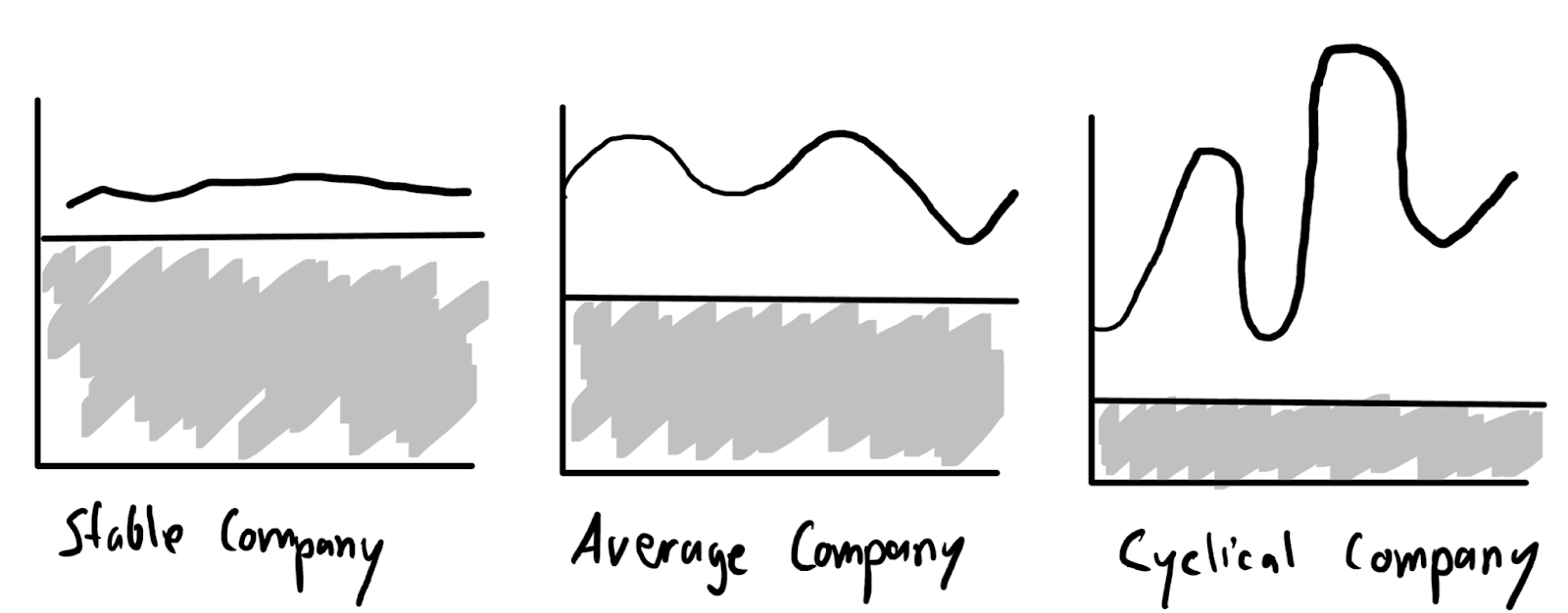

Stable, Average, or Cyclical?

In another memo called “Volatility + Leverage = Dynamite”, Howard Marks uses a fantastic illustration to answer the question: “How much leverage is optimal?”

Howard Marks uses three types of companies: Stable, average, and cyclical companies.

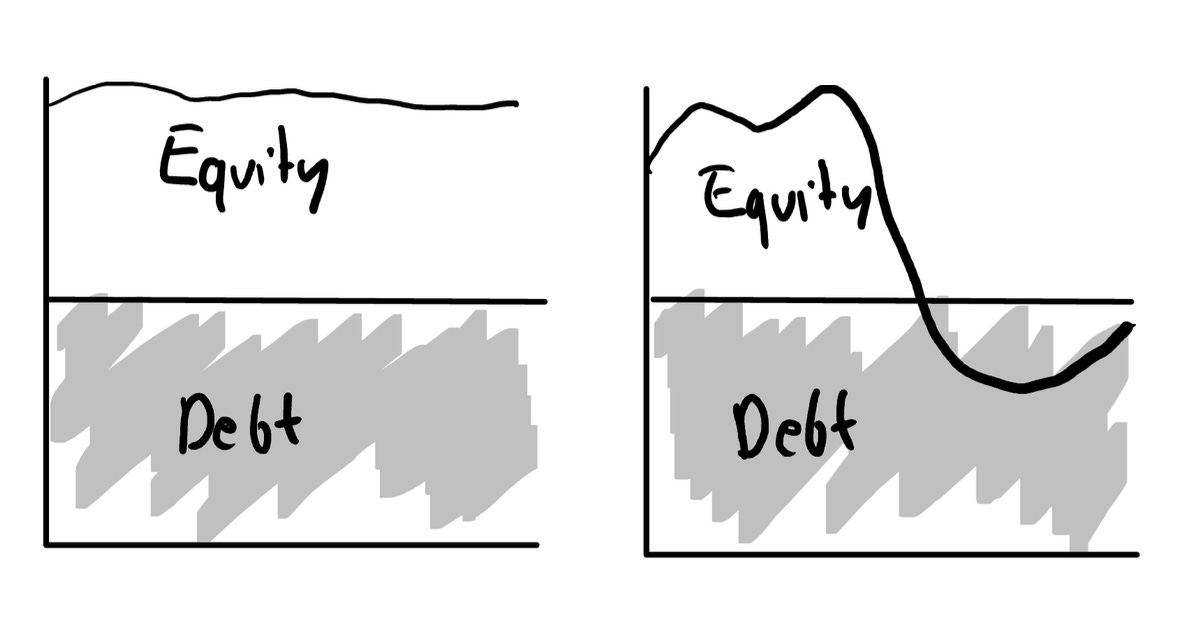

Howard Marks illustrates the financial structure of a company in a similar way.

By combining both concepts, the company must not cross the bottom line in order to avoid bankruptcy. The financial structure must be so that its value doesn’t wall below the equity and into the debt. While “naive and far-from technically correct terms”, when the amount of debt exceeds the value of the company, it is insolvent.

This illustration shows that the optimum leverage is different for each type of company, as each company has a different level of riskiness and volatility.

Stable Companies

Highly leveraged business models are not inherently risky if the underlying assets and revenue streams are stable and predictable.

This is the case with utility companies, which, due to their regulated profit margins tied to stable asset bases, can sustain higher levels of debt. Similarly, life insurance companies operate under the premise of predictable risk, with actuarial data providing clear insights into life expectancy. Also, companies in regulated healthcare markets like Germany can manage higher leverage effectively, as they have predictable revenue streams due to regulatory frameworks and consistent demand in an aging society.

Depending on the country, other examples of stable companies may also include telecommunications, pharmaceutical manufacturers, public transport providers, and renewable energy suppliers with long-term contracts and subsidies.

Average Companies

For average companies, which neither enjoy the predictability of stable companies nor face the high volatility of cyclical ones, the approach to leverage must be more nuanced. These companies often operate in competitive markets with moderate fluctuations in demand and revenue. Examples include mid-sized retail chains, software development firms, and general manufacturing businesses.

Their revenue streams, while not as volatile as cyclical companies, do not guarantee the same level of stability as utilities or insurance firms. Therefore, average companies must carefully calibrate their debt levels, ensuring they maintain enough flexibility to capitalize on growth opportunities without overextending themselves financially. Optimal leverage for these companies involves a balance that allows for strategic investments and expansion while keeping debt at manageable levels to avoid undue financial strain during market downturns.

Cyclical Companies

Cyclical companies, such as those in the construction, automotive, and luxury goods sectors, experience significant fluctuations in demand and revenue in line with economic cycles. The inherent volatility of their markets makes high leverage a risky proposition, as downturns can drastically reduce their revenue and impair their ability to service debt. For these companies, maintaining lower levels of leverage is crucial to surviving economic downturns.

Optimal debt usage involves leveraging up during the early stages of economic recovery to finance expansion and capitalizing on upswings, while deleveraging in anticipation of economic downturns. This strategy requires a keen understanding of market cycles and the discipline to reduce debt even when times are good, to buffer against the inevitable lean periods that cyclical companies face.

The Skywert Perspective

From our Skywert perspective, the US debt crisis is a significant threat that cannot be ignored. The national debt has surged to unprecedented levels, and the government's reliance on debt to finance its spending is unsustainable in the long term. While it is difficult to predict the exact timing of a debt crisis, the likelihood of such an event occurring is high. However, it is also important to consider the potential for technological advancements, particularly in artificial intelligence (AI), to drive massive productivity gains and innovation in the US economy. These advancements could postpone the debt crisis for several years, potentially even a decade, by boosting economic growth and increasing tax revenues.

Despite this potential reprieve, the underlying debt situation remains dire. The only viable long-term solutions appear to be significantly higher inflation or the replacement of the US dollar as the world's reserve currency. The US government is likely to have a strong motivation to maintain its status as the issuer of the global reserve currency, which could lead to the introduction of a fixed supply digital currency. However, trust in the US dollar and the US government is likely to continue declining, adding to the uncertainty.

In this context, leverage can still be a useful tool for growth, but it must be employed judiciously. Stable companies with strong cash flows and the ability to pass on cost increases to consumers are well-positioned to handle higher leverage. Additionally, companies that stand to benefit significantly from exponential technologies, such as those involved in AI, robotics, and biotechnology, offer promising opportunities. While the core technology developers are typically funded by venture capital, supplementary companies that supply the infrastructure and services needed to support these technologies can be acquired at fair valuations today. These companies, if purchased at a reasonable price and creatively structured, can provide a hedge against inflation through substantial equity growth over the next decade.

For example, consider a company that provides cloud infrastructure products and services essential for AI development. Acquiring such a company with a mix of debt and equity financing can be a strategic move. The debt can be structured with flexible terms, such as interest-only payments for the initial years, to allow the company to reinvest its cash flows into growth initiatives. Additionally, earn-out provisions can be included to align the interests of the sellers with the future performance of the company, reducing the upfront cash outlay and mitigating risk.

While the mainstream narrative may focus on the risks of leverage in an uncertain economic environment, there are opportunities for those willing to think differently. Especially investing in companies that are not only stable but also positioned to benefit from technological advancements can provide a unique edge. These companies are likely to experience significant growth as they capitalize on the increasing demand for their products and services driven by exponential technologies.

Creative Deal Structuring

At Skywert, we believe investors must approach the use of leverage in acquisitions with a combination of caution, creativity, and strategic foresight. While traditional earn-out structures can help bridge valuation gaps and align interests between buyers and sellers, investors should embrace innovative and creative ways to structure deals that can maintain healthy leverage and make deals happen.

One innovative strategy is to implement a dynamic earn-out structure that adjusts based on the target company's performance relative to the broader economic environment. For example, the earn-out could be tied to the company's revenue growth or profitability compared to industry benchmarks or macroeconomic indicators. This approach would ensure that the seller is rewarded for strong performance while also protecting the buyer from overpaying in the event of an economic downturn.

Another unique deal structure could involve a hybrid financing model that combines traditional debt with revenue-based financing. In this scenario, a portion of the acquisition price would be funded through a conventional leveraged loan, while the remainder would be financed through a revenue-sharing agreement. The seller would receive a percentage of the target company's future revenue until a predetermined threshold is met. This structure aligns the interests of both parties, as the seller is incentivized to support the company's growth, and the buyer benefits from reduced upfront debt and lower fixed obligations.

Alternatively, a deal could be structured with a built-in refinancing option triggered by specific milestones or market conditions. For instance, the initial acquisition could be financed with a relatively conservative level of debt, but the agreement could include provisions for additional debt to be raised if the company achieves certain growth targets or if interest rates decline. This approach allows the buyer to optimize the capital structure over time while reducing the risk of overleverage at the outset.

Investors could explore a phased acquisition model that combines an initial minority stake with an option to acquire a controlling interest at a later date. The initial investment would be funded primarily with equity, allowing the buyer to gain a foothold in the company and work closely with management to drive growth. The option to acquire a controlling stake would be contingent upon the company achieving specific performance milestones, and the purchase price could be determined using a predetermined formula based on financial metrics. This structure reduces the upfront debt burden while providing the buyer with a clear path to control and the seller with a compelling incentive to maximize value.

Lastly, another creative structure is a shared upside model, where the seller receives a portion of the equity in the acquired company, but with a twist. The seller's equity stake would be subject to a "ratchet" mechanism, whereby their ownership percentage would increase if the company achieves certain performance targets. This structure aligns the interests of the seller with those of the buyer, as both parties benefit from the company's success. Additionally, it allows the buyer to conserve cash and reduce leverage, as a portion of the purchase price is paid in equity rather than debt.

In conclusion, the use of leverage in the current environment requires a delicate balancing act between opportunism and prudence, between caution, creativity, and strategic foresight. By embracing innovative deal structures, investors can navigate the challenges of the current economic environment and unlock value in a wide range of transactions. Through a combination of thoughtful financial engineering, risk-sharing mechanisms, and performance-based incentives, investors can structure deals that leverage debt responsibly, drive growth, and deliver attractive returns in the face of economic uncertainty.